By Intan Suwandi, R. Jamil Jonna and John Bellamy Foster (originally posted at Monthly Review),

Twenty-first-century capitalist production can no longer be understood as a mere aggregation of national economies, to be analyzed simply in terms of the gross national products (GDPs) of the separate economies and the trade and capital exchanges occurring between them. Rather, it is increasingly organized in global commodity chains (also known as global supply chains or global value chains), governed by multinational corporations straddling the planet, in which production is fragmented into numerous links, each representing the transfer of economic value. With more than 80 percent of world trade controlled by multinationals, the annual sales of which now equal around half of global GDP, these commodity chains can be seen as fastened at the center of the world economy, connecting production, located primarily in the global South, to final consumption and the financial coffers of monopolistic multinational firms, located primarily in the global North.1

The commodity chain of General Motors includes twenty thousand businesses worldwide, mostly in the form of parts suppliers. No U.S. automobile manufacturer imports less than around 20 percent of its parts from abroad for any of its vehicles, with imported parts sometimes amounting to around 50 percent or more of the assembled vehicle.2 Likewise, Boeing purchases from abroad about a third of the parts it uses for its aircraft.3 Other U.S. companies, such as Nike and Apple, offshore their production to subcontractors, mainly in the periphery, with production carried out according to their exact, digital specifications—a phenomenon known as arm’s length contracting, or what is sometimes referred to as non-equity modes of production. This offshoring of production by today’s multinational corporations in the center of the world economy has led to a vast shift in the predominant location of industrial employment, from the global North up through the 1970s to the global South this century.4

Studies have found that the accelerating pace of offshoring is closely related to foreign direct investment (FDI) in low-wage areas in the periphery, associated with intrafirm trade. In 2013, the global FDI inflows to “developing economies” reached a record high of 52 percent of total FDI, “exceeding flows to developed economies for the first time ever, by $142 billion.”5 But of equal importance today is arm’s length contracting. The World Bank, using U.S. Census data, indicates that 57 percent of all U.S. trade is arm’s length trade, while a rapidly growing part of this is taking the form of monopolistic arm’s length contracting, involving specified production carried out by subcontracting firms (such as the Taiwanese Foxconn operating in China) producing commodities (such as iPhones) for buyer-driven multinational corporations (such as Apple). In general, the lower the per-capita income of a U.S. trading partner, the higher the share of U.S. arm’s length trade, indicating that this is all about low wages.6 Even multinationals with high levels of FDI are heavily involved in arm’s length trade, moving in this way between direct and indirect exploitation. Arm’s length contracts generated about $2 trillion in sales in 2010, “much of it in developing countries.”7 In 2010–14, the world economy grew at a 4.4 percent rate while arm’s length trading grew at a 6.6 percent rate, far exceeding the former.8

Although these phenomena are not entirely new, in the sense that all sorts of historical precedents can be found in the operations of international corporations, the scale and sophistication of commodity chains today represent qualitative changes that are transforming the character of the entire global political economy. This has generated enormous confusion in political-economic analyses on both the right and the left. Thus, the shift in industrial employment and the rapid growth of some countries in the periphery, particularly in East Asia, led even as important a Marxist theorist as David Harvey to conclude that the direction of imperialism has somehow reversed, with the West, or the global North, now on the losing end. As he puts it, “the historical draining of wealth from East to West for more than two centuries has…been largely reversed over the last thirty years.… I think it is useful to take up Giovanni Arrighi’s preference to abandon the idea of imperialism (along with the rigidities of the core-periphery model of world system theory) in favor of a more fluid understanding of competing and shifting hegemonies within the global state system.”9

Yet, such assessments are based on the illusion that twenty-first-century imperialism can be approached, as in earlier periods, mainly on the level of the nation-state without a systematic investigation of the increasing global reach of multinational corporations or the role of the global labor arbitrage, sometimes referred to in business circles as low-cost country sourcing. At issue is the way in which today’s global monopolies in the center of the world economy have captured value generated by labor in the periphery within a process of unequal exchange, thus getting “more labour in exchange for less.”10 The result has been to change the global structure of industrial production while maintaining and often intensifying the global structure of exploitation and value transfer.

The complexity of the world employment situation generated by global commodity or supply chains is indicated in Table 1, which includes the countries with the largest shares of employment in global commodity chains in 2008 and/or 2013.

Table 1. Countries with the Highest Proportion of Global Supply Chain Jobs (GSC Jobs), and their Primary Export Destination

| 2008 | 2013 | |||

| Country | Share of All GSC Jobs | Primary Export Destination | Share of All GSC Jobs | Primary Export Destination |

| China | 43.4% | United States | 39.2% | United States |

| India | 15.8% | United States | 16.8% | United States |

| Indonesia | 4.6% | Japan | 4.6% | China |

| Russian Federation | 4.1% | Germany | 4.1% | China |

| Brazil | 3.5% | United States | 4.1% | China |

| Germany | 3.4% | France | 3.6% | China |

| United States | 3.3% | Canada | 3.6% | China |

| Japan | 2.3% | United States | 1.9% | China |

| Mexico | 1.8% | United States | 2.2% | United States |

| South Korea | 1.7% | United States | 2.1% | China |

| United Kingdom | 1.7% | United States | 1.9% | United States |

| Total | 85.6% | 84.2% |

Source: This is a modified version of data taken from Table 2 of Takaaki Kizu, Stefan Kühn, and Christian Viegelahn. 2016. “Linking Jobs in Global Supply Chains to Demand,” ILO (International Labour Organization) Research Paper, Geneva, 15.Notes: The “Share of All GSC Jobs” is relative to the 40 countries in the WIOD (World Input-Output Database) series. The “Primary Export Destination” is defined as the country to which the majority of the output of a given country’s GSC Jobs is exported. The WIOD input-output tables even account for the economic activity of countries outside the dataset (categorized as, “rest of world”). Yet, it should be noted that these 40 countries (43 in the 2016 Release) account for the lion’s share both of world income and GSC Jobs.

As Table 1 shows, China and India provide by far the largest share of the total employment engaged in global commodity chains, while, for both countries, the United States is the primary export destination. This creates a situation where production and consumption in the world economy are increasingly severed from each other. Moreover, value added, associated with such commodity chains, as we shall see, is disproportionately attributed to economic activities in the wealthier countries at the center of the system, although the bulk of the labor occurs in the poorer nations of the periphery or the global South.

Economic researchers at the Institut de Recherches Économiques et Sociales in France indicate that global commodity chains have three different elements: (1) a production element linking parts and commodities in complex production chains; (2) a value element, which focuses on their role as “value chains,” transferring value between and within firms globally; and (3) a monopoly element, reflecting the fact that such commodity chains are controlled by the centralized financial headquarters of monopolistic multinational corporations and garner massive monopoly rents, as theorized by Stephen Hymer in the 1970s.11 The common distinction between global supply chains and global value chains is mainly between what Karl Marx called the material or “natural form” of the commodity, its use value, as opposed to its “value form,” or exchange value. All of this, however, needs to be united within a general theory of global commodity production.12

In this analysis of global commodity chains, the use-value and exchange-value aspects are brought together through recognition of both the material (supply) and value aspects.13 As in all capitalist production, the value component is dominant in such commodity chains and is rooted in the exploitation of labor. We therefore focus our analysis on the theoretical and empirical analysis of what we term labor-value commodity chains, emphasizing the exchange-value (value-form) element, without ignoring the material or use-value (natural-form) element. In this way, we seek to understand how the new imperialism of the global labor arbitrage works and how value, derived from low-wage labor in the periphery, is being captured globally.

Utilizing a publicly available database of world economic activity, we construct a series on unit labor costs incorporating both labor productivity and wage levels.14 The goal is to develop a theoretically consistent methodology—rooted in labor-value relations—for making cross-national comparisons of labor exploitation, thereby building a theoretical and empirical basis for commodity-chain analysis. We conceive of each link or node in a commodity chain in terms of unit labor costs, which largely determine profit margins, with the critical nodes of production being those in which labor costs are most concentrated and thus involve the greatest amount of socially necessary labor—as at the point of assembly of the product.

Examination of unit labor costs of key countries in both the center and the periphery of the world economy demonstrates that, in twenty-first-century imperialism, multinational corporations are able to carry out a process of unequal exchange in which they get, in effect, more labor for less, while the excess surplus obtained is often misleadingly attributed to “innovative,” financial, and value-extractive economic activities taking place at the center of the system. Indeed, much of the immense value capture associated with the global labor arbitrage circumvents production in the center economies, at the expense of workers there who have seen their jobs offshored. This has contributed to the amassing of vast pyramids of wealth disconnected from economic growth in the center economies themselves.15 Much of this draining of value from the periphery takes the form of unrecorded illicit flows. According to one recent pioneering study of global financial flows by the Centre for Applied Economics of the Norwegian School of Economics and the United States-based Global Financial Integrity, net resource transfers from developing and emerging economies to rich countries were estimated at $2 trillion in 2012 alone.16

Huge quantities of this loot captured from peripheral economies in the global South ends up being parked in the “treasure islands” of the Caribbean where trillions of dollars of money capital are now deposited, outside of the tax and accounting apparatuses of even the most powerful nation-states.17 Such financial expropriation characterizes the whole era of monopoly-finance capital, in which the growing role of what Marx, following James Steuart, called profit by expropriation (or profit by alienation) is now evident.18 This is clear in the increasing role of value capture and value extraction, as opposed to direct value generation, in determining the profits of multinational firms.19

What is clear is that the globalization of production is built around a vast chasm in unit labor costs between center and periphery economies, reflecting much higher rates of exploitation in the periphery. This reflects the fact that the difference in wages is greater than the difference in productivity between the global North and the global South.20 Our data shows that the gap in unit labor costs in manufacturing between key core (United States, United Kingdom, Germany, and Japan) and key periphery emerging states (China, India, Indonesia, and Mexico) has been on the order of 40–60 percent during most of the last three decades. This enormous gulf between global North and global South arises from a system that allows for the free international mobility of capital, while tightly restricting the international mobility of labor.21 The result is to hold wages down in the periphery and to make possible the enormous siphoning off of economic surplus from the countries of the South. As Utsa Patnaik and Prabhat Patnaik have argued, the drain of surplus from the periphery “refers not just to the direction of capital flows but to the phenomenon of sucking out the surplus of an economy without any quid pro quo.”22

The term supply chain is often used to refer to “a sequence of production operations,” which begins “at conception and development of the product or system, goes through the production process including acquisition of inputs (raw materials, tools, equipment), and finishes with distribution, maintenance and the end of the product’s life [or its consumption]. The parts and modules produced at each step of the process are assembled to make a final product.”23

Global commodity chains can then be seen as

integrated global spaces created by financial groups with manufacturing activities. Such spaces are global in that they open up a strategic horizon for augmenting the value of capital that reaches far beyond national borders and undermines national regulations. Such spaces are integrated in that they are made up of hundreds, even thousands, of subsidiaries (production, R&D [research and development], finance, etc.) whose activities are coordinated and controlled by a central body (the parent company or a holding company) that manages resources to ensure that the capital valorisation process is profitable both financially and economically.24

The participation of countries in such global commodity chains has a profound impact on labor. This can be seen from the rapid increase in the number of jobs related to global commodity chains, from 296 million workers in 1995 to 453 million in 2013. This growth in commodity-chain production is concentrated in “emerging economies” where such job growth reached an estimated 116 million from 1995 to 2013, with manufacturing as the predominant sector and directed at exporting to the global North.25 In 2010, 79 percent of the world’s industrial workers lived in the global South, compared to 34 percent in 1950 and 53 percent in 1980.26 Manufacturing has become “the chief source of the third world’s dynamism” both in exports and in production, especially in East and Southeast Asia, where, by 1990, the manufacturing share of GDP was higher than that of other regions.27 A report by the Asian Development Bank shows that most countries in Southeast Asia, particularly those that are considered developing, experienced an increase in their manufacturing output shares from the 1970s to the 2000s.28

Exploring this complex reality has posed challenges to social scientists. Marx had written in Capital of “the general chain of metamorphoses [with respect to both use value and exchange value] taking place in the world of commodities.” Later, following Marx, Rudolf Hilferding in Finance Capital referred to “link[s] in the chain of commodity exchanges.”29 Inspired by these earlier Marxian notions of chains of commodity exchanges characterizing the capitalist world economy, Terence Hopkins and Immanuel Wallerstein advanced the commodity chain concept in the 1980s as part of the world-systems perspective—with an emphasis on the “historical reconstruction of industries during the long sixteenth century.”30 The global commodity-chain framework was further popularized in the mid–1990s, marked by the publication of Commodity Chains and Global Capitalism, edited by Gary Gereffi and Miguel Korzeniewicz.31 Later, Gereffi also became a prominent figure in the forming of the global value-chain/global supply-chain research network in 2000. This research network was created in the hope of uniting several different but similar approaches to global chain studies.32 Although the global value-chain/supply-chain framework itself was inspired by the early research on global commodity chains, it was frequently to become integrated with the neoclassical tradition of transaction-cost economics.33

In introducing the concept of the commodity chain, Hopkins and Wallerstein defined it as “a network of labor and production processes whose end result is a finished commodity.”34 Such chains are usually “geographically extensive and contain many kinds of production units within them with multiple modes of remunerating labor.”35 Commodity-chain scholars use the term nodes to refer to separable processes that constitute a commodity chain. In this context, a node signifies a particular or specific production process and each node within a commodity chain involves “the acquisition and/or organization of inputs (e.g., raw materials or semifinished products), labor power (and its provisioning), transportation, distribution (via markets or transfers), and consumption.”36 Today, international commodity production more and more assumes the form of sophisticated labor-value commodity chains, with higher levels of organization. Center economies thus increasingly rely on imported inputs of goods and services (including assembly) from low-income countries.37 As is now universally recognized, one of the striking features related to such commodities is a “very large and growing proportion of the workforce…located in developing economies.”38

William Milberg and Deborah Winkler argue that a shift in corporate strategy is a key driver in this “new wave” of globalization. The strategy involves a search for lower costs and greater flexibility, as well as a desire to “allocate more resources to financial activity and short-run shareholder value while reducing commitments to long term employment and job security.”39 Further, Gereffi emphasizes the emergence of major multinational corporations that do not manufacture their own products, which he claims is central to the “new trends” of offshoring. Such corporations, which are usually large retailers and branded marketers, can be referred to as the new drivers in the global chains that have become more prominent over the last couple of decades.40 Arm’s length production by multinational corporations—of which Nike and Apple are perhaps the best-known examples—is associated with governance structures in which corporations, usually situated at the center of the world economy, play a pivotal role in setting up dispersed production networks in exporting countries, typically in the third world.41 They are actually not real manufacturers, but merely merchandisers, that is, companies that “design and/or market, but do not make, the branded products they sell.”42

Popular discussions of arm’s length corporate contracting highlight the “decentralized characteristic” of such chains in the sense of the geographic dispersal of production. Yet, far from representing actual decentralization of control over production (and valorization), as is sometimes assumed, the “dispersed” commodity chains associated with a given multinational with no equity in the various production segments that it has subcontracted out, are crucially governed by its centralized financial headquarters. The financial headquarters of a multinational retains monopolies over information technology and markets, and appropriates the larger portion of the value added in each link in the chain. Despite China’s reputation as the largest exporter of high-technology goods, economist Martin Hart-Landsberg points out that 85 percent of the country’s high-technology exports are mere links or nodes in the global commodity chains of multinationals.43 As Hymer said a few decades ago: the headquarters of multinationals “rule from the tops of skyscrapers; on a clear day, they can almost see the world.”44

As John Bellamy Foster, Robert W. McChesney, and R. Jamil Jonna argue, arm’s length contracts actually allow firms to capture “extremely high profit margins through their international operations and [exert] strategic control over their supply lines—regardless of their relative lack of actual FDI.”45 But this is frequently difficult to examine since, in such a practice, multinational corporations often have only an indirect connection with the workers/farmers who produce their goods. There are no visible flows of profits from these foreign subcontractors to their global North customers—multinationals. As John Smith notes with respect to arm’s length contracting:

Not a single cent of H&M’s, Apple’s or General Motors’ profits can [in the usual value-added accounting] be traced back to the super-exploited Bangladeshi, Chinese and Mexican workers who toil for these TNCs’ (Transnational Corporations) independent suppliers, and it is this “arm’s length” relationship which increasingly prevails in the global value chains that connect TNCs and citizens in imperialist countries to the low-wage workers who produce more and more of their intermediate inputs and consumption goods.46

Empirical analysis that accounts for the full impact of the global labor arbitrage thus becomes doubly difficult.

However, a closer look at the logic behind these forms of offshoring will allow us to see the labor-value commodity chains and power relations embedded in them.47 The question is not merely about how the multinationals govern commodity chains, but also how they facilitate the extraction of surplus from the global South. This is captured in the concept of the global labor arbitrage, famously defined by Stephen Roach, the former chief economist of Morgan Stanley, as the replacement of high-wage workers in the United States and other rich economies “with like-quality, low-wage workers abroad.”48 Here, the global labor arbitrage is rationalized as “an urgent survival tactic” for companies in the global North, pressured by the need to cut costs and to “search for new efficiencies.”49

Upon critical examination, this cost-control imperative is none other than a form of arbitrage, taking advantage of price differentials, in this case with respect to wages, within the imperfect global market—based on the unequal freedom of movement of capital and labor.50 Although labor is still largely constrained within national borders due to immigration policies, global capital and commodities have far more freedom to move around, further heightened in recent years due to trade liberalization. The global labor arbitrage thus serves as a means for multinationals to benefit from the “enormous international differences in the price of labor.”51

Viewed through a critical political-economy perspective, then, the global labor arbitrage is the overexploitation of labor in the global South by international capital. It constitutes unequal exchange, understood as the exchange of more labor for less, in which monopoly-finance capital at the center of the system benefits from high markups on low-cost labor in the global South. The process of unequal exchange at the same time marks the further incorporation of the global South countries into the global economy.52

In the context of the Marxian labor theory of value, the global labor arbitrage is a quest for valorization. It is a strategy for both reducing socially necessary labor costs and maximizing the appropriation of surplus value. It extracts more out of workers through various means, including repressive work environments in periphery-economy factories, state-enforced bans on unionization, and quota systems or piece-rate work.

The global labor arbitrage is made possible in part by what Marx refers to as the industrial reserve army of the unemployed—which in this case is on a global scale, thus a global reserve army of labor.53 The creation over the last few decades of a much larger global reserve army is partly connected to the “great doubling” phenomenon, which refers to the integration of the workforce of former socialist countries (including China) and formerly heavily protectionist countries (such as India) into the global economy, with the resulting expansion of the size of both the global labor force and its reserve army.54 Also central to the creation of this reserve army is the depeasantization of a large portion of the global periphery through the spread of agribusiness.55 This forced movement of peasants from the land has resulted in the growth of urban slum populations.56 Marx connected the “freeing” of peasants (the “latent” part of the reserve army) from the land to the process of “so-called primitive accumulation.”57

Reproducing the global reserve army of labor not only serves to increase shorter-term profits; it serves as a divide-and-rule approach to labor on a global scale in the interest of long-term accumulation by multinationals and the state structures aligned with them.58 Although competition among corporations is limited to oligopolistic rivalry, competition among workers of the world (especially those in the global South) is greatly intensified by increasing the relative surplus population. This divide-and-rule strategy serves to integrate “disparate labor surpluses, ensuring a constant and growing supply of recruits to the global reserve army” who are “made less recalcitrant by insecure employment and the continual threat of unemployment.”59

It follows from the above discussion that the freely competitive model has been made obsolete. Nevertheless, the “traditional” rule of fighting for low-cost production is still alive and well. Indeed, one may argue that it is intensified in the age of monopoly-finance capital. The goal of multinationals is always the creation and the perpetuation of monopoly power and monopoly rents, that is, “the power to generate persistent, high economic profits through a mark-up on prime production costs.”60 As production becomes globalized, Zak Cope writes, “the leading oligopolies compete to reduce labor and raw materials costs. They export capital to the underdeveloped countries in order to secure a high return on the exploitation of abundant cheap labor and the control of economically pivotal natural resources.”61 Whether through intrafirm trade or arm’s length contracts, the increasing trend of offshoring in the last few decades constitutes a continuation of the imperialistic projects of multinationals, with which the states in the Triad of the United States and Canada, Europe, and Japan are fully compliant.

This general understanding of globalized production as a process of unequal exchange and imperial hierarchies can be concretized by empirical analyses that help demonstrate how participation of countries in global commodity chains relates to changes in unit labor costs. As we shall see in the following section, unit-labor cost data can help formulate a labor-value commodity chain analysis that puts labor at its center, aimed at understanding differential rates of labor exploitation and their relation to the globalization of production.

Grounding the Labor Value-Commodity Chains Approach: An Empirical Model

A chapter in the 2015 International Labour Organization (ILO) report on world employment is dedicated to how changes in global production patterns influenced firms and employment. It notes that the number of jobs related to global commodity chains increased sharply between 1995 and 2013, with about one in five jobs worldwide estimated to be linked to global commodity chains and with more notable increases in the manufacturing sector of so-called emerging economies. Interestingly, the report also found that, while participation in global commodity chains positively influences firms’ productivity and profitability, it does not have a commensurate positive effect on wages. This increase in productivity and the absence of any commensurate positive impact on wages means that participation in global commodity chains leads to a drop in “the portion of value added that goes to workers”—indeed, the report concludes, “this is the result when relating GSC [global supply chain] participation directly to the wage share in both emerging and developed economies” (our italics).62

A comparison of national differences in unit labor cost—a measurement of the labor cost to produce one unit of a product—gets at the same underlying issues as raised by the ILO, but in terms that aim at uncovering gross profit margins or the rate of surplus value. Unit labor costs combine productivity with wage costs in a manner closely related to the treatment of labor costs in Marx’s theory of exploitation.63 Unit labor cost is a composite measure, combining data on labor productivity and compensation to assess the price competitiveness of a given set of countries. It is typically presented as the average cost of labor per unit of real output, or the ratio of total hourly compensation to output per hour worked (labor productivity). Although unit labor cost data can be compiled for the economy as a whole, most analysts narrow the focus to the manufacturing sector to improve comparability.

Unit labor costs can be seen as a more comprehensive indicator—compared to labor-productivity growth rates—of international competitiveness.64 In a capitalist economy, neither relative productivity measures nor relative wages are adequate by themselves in analyzing the respective positions of various capitalist economies: unit labor costs combine both sets of data. For example, a country with a higher rate of productivity growth may lose out in the competitive race to a country that has a somewhat lower rate of productivity growth, but also lower wage costs. Conversely, a country with lower wage costs may lose out in the competitive race to a country with higher productivity growth. By combining both sets of data, unit labor costs also reveal where gross profit margins—which, in Kaleckian terms, represent the markup (an indication of the degree of monopoly) on direct production costs—will be the widest.65

In an article on intercapitalist competition, arising out of a debate with Robert Brenner, Foster used the average annual rate of change in unit labor costs (in manufacturing) to compare the Group of Seven (G7) countries in two periods, ranging from 1985 to 1998.66 The data showed slower growth of unit labor costs in the United States than in other G7 countries during the period, a fact that gave the United States, as concluded by the Bureau of Labor Statistics’ analysts, a “decisive advantage” in “overall competitive position over its major competitors in the period after 1985,” despite its somewhat lower levels of actual productivity growth. This, Foster contended, reflected the “effectiveness of the class struggle against labor in the United States.”67

This finding suggests that it would be useful to elaborate on what changes in unit labor costs can tell us about “capturing value” from labor in the global South through offshoring practices. We are interested in determining how changes in unit labor costs over time relate to countries’ participation in global commodity chains, and how this relationship can help explain the extraction of surplus from the global South.

To investigate the connection between unit labor cost and global commodity chains, we construct an original dataset using the World Input Output Database (WIOD), which was recently made publicly available.68 The power of this set of data was showcased in the 2015 edition of the ILO’s “World Employment and Social Outlook,” which focused on measurement of the extent of global commodity chains. The WIOD dataset contains information on over forty countries from 1995 to 2016, covering 85 percent of world GDP and, crucially, includes key countries from the global South, such as China, India, Indonesia, and Mexico.69 Combining it with data from the Socio Economic Accounts (SEA, a subset of the WIOD database) makes it possible to construct comprehensive cross-national measures of hourly wages per unit labor cost.70 We focus attention on eight countries with high levels of participation in global commodity chains—the United States, United Kingdom, Germany, Japan, China, India, Indonesia, and Mexico.

In order to understand the significance of data on unit labor costs, it is useful to look first at a comparison of hourly compensation in dollar terms, which points to the vast discrepancies in wage levels internationally between the global North and the global South. Although it is common to look at hourly compensation in terms of purchasing power parity (PPP$, equivalent ability to purchase goods and services), which is useful for looking at issues of equity, we are interested in questions of surplus extraction and value capture from the standpoint of multinational corporations headquartered in the center of the system. From that perspective, U.S. dollars as the hegemonic currency are central to the overall “value of money” and the amassing of monetary wealth on a world scale.71 It is labor costs, measured in market dollars, which largely determines the overall profit margins of multinationals.

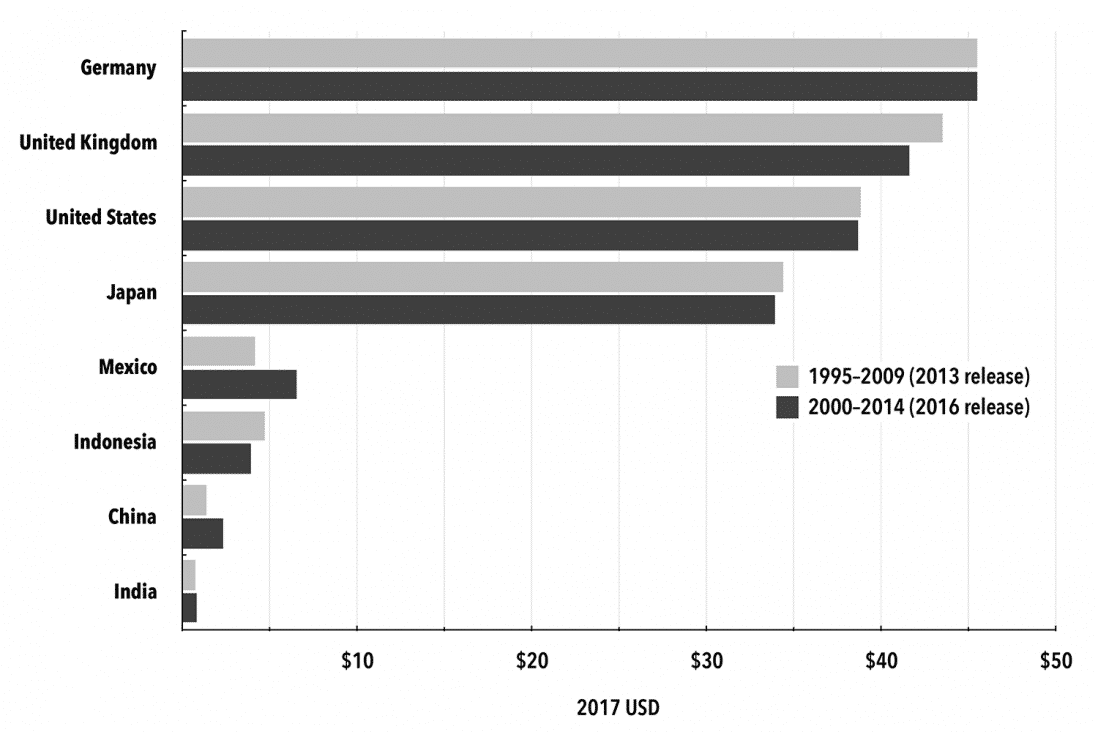

Chart 1, which reports average hourly labor compensation in manufacturing industries in 2017 U.S. dollars, illustrates the wage chasm that exists between economies of the global North and global South. The data show that there is a massive discrepancy in wage levels between center (global North) and periphery (global South). Here, hourly compensation is converted into actual dollars—representing the hegemonic foreign exchange/reserve currency determining the purchase price of labor, profit margins, and international financial flows—rather than applying a purchasing power parity conversion (see Statistical Appendix).

Chart 1: Average Hourly Compensation in Manufacturing, 2017 USD

Sources: WIOD: Socio Economic Accounts (SEA), Release 2013 and 2016. Marcel P. Timmer, Erik Dietzenbacher, Bart Los, Robert Stehrer, Gaaitzen J. de Vries (2015), “An Illustrated User Guide to the World Input–Output Database: The Case of Global Automotive Production,” Review of International Economics, 23: 575–605; Exchange Rates: “The Next Generation of the Penn World Table,” Robert C. Feenstra, Robert Inklaar, Marcel P. Timmer, American Economic Review 2015; USD Conversion Factors: “Individual Year Conversion Factor Tables,” Robert Sahr, Oregon State University 2019.Notes: Figures exclude the UK industry “Coke and refined petroleum products.” Also see Statistical Appendix.

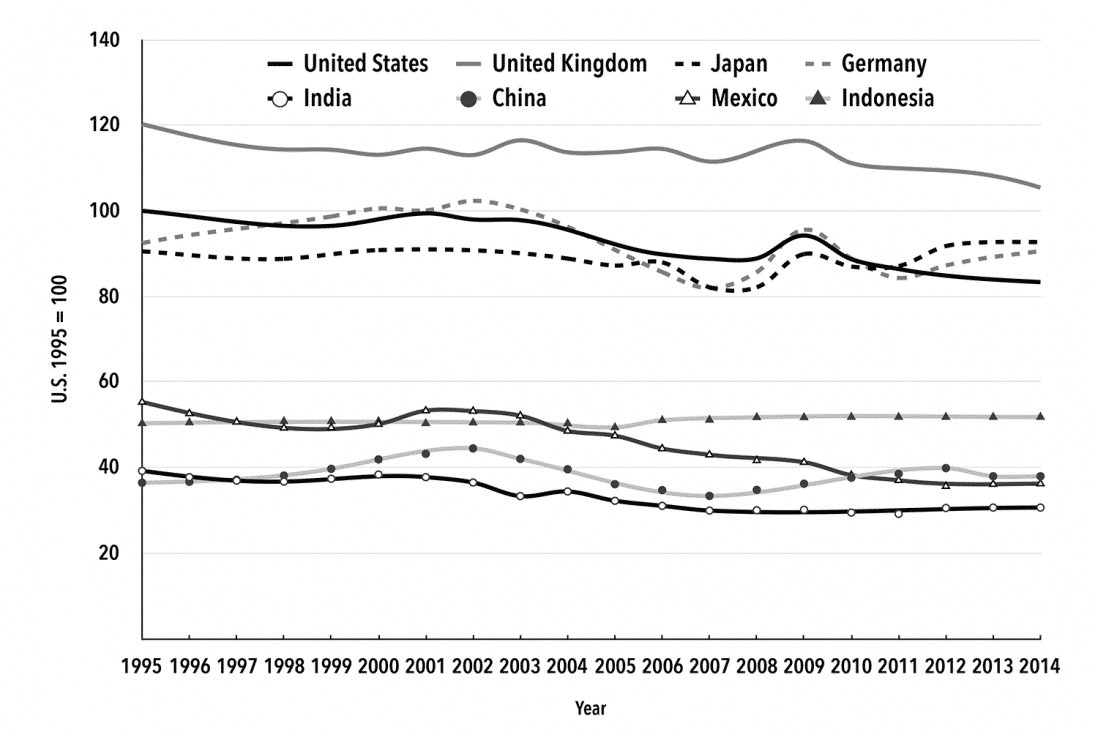

The much higher rates of exploitation of workers in the global South has to do not simply with low wages, but also with the fact that the difference in wages between the North and South is greater than the difference in productivity. Chart 2 presents an index of unit labor costs in a number of key core developed and periphery emerging countries accounting for significant shares of GSC jobs in the global economy between 1995 and 2014—a period stretching from the development of the high-tech bubble of the 1990s to the Great Financial Crisis of 2007–09 to the early years of recovery from the crisis.72 The chart shows the huge gap that exists between unit labor costs in manufacturing in the advanced industrial economies in the global North and the emerging economies in the global South. The four advanced industrial economies (United States, United Kingdom, Germany, and Japan) are fairly tightly clustered together, while all four have much higher unit labor costs than the four emerging economies (China, India, Indonesia, and Mexico).

Chart 2: Index of Average Unit Labor Costs in Manufacturing, Selected Countries, 1995–2014 (U.S. 1995 = 100)

Sources: WIOD: SEA, Release 2013 and 2016. Timmer, et. al., “An Illustrated User Guide to the World Input–Output Database: the Case of Global Automotive Production,” Review of International Economics, 23: 575–605.Notes: Unit labor cost is given by the ratio of total labor compensation per hour to gross output per hour. Also see Statistical Appendix.

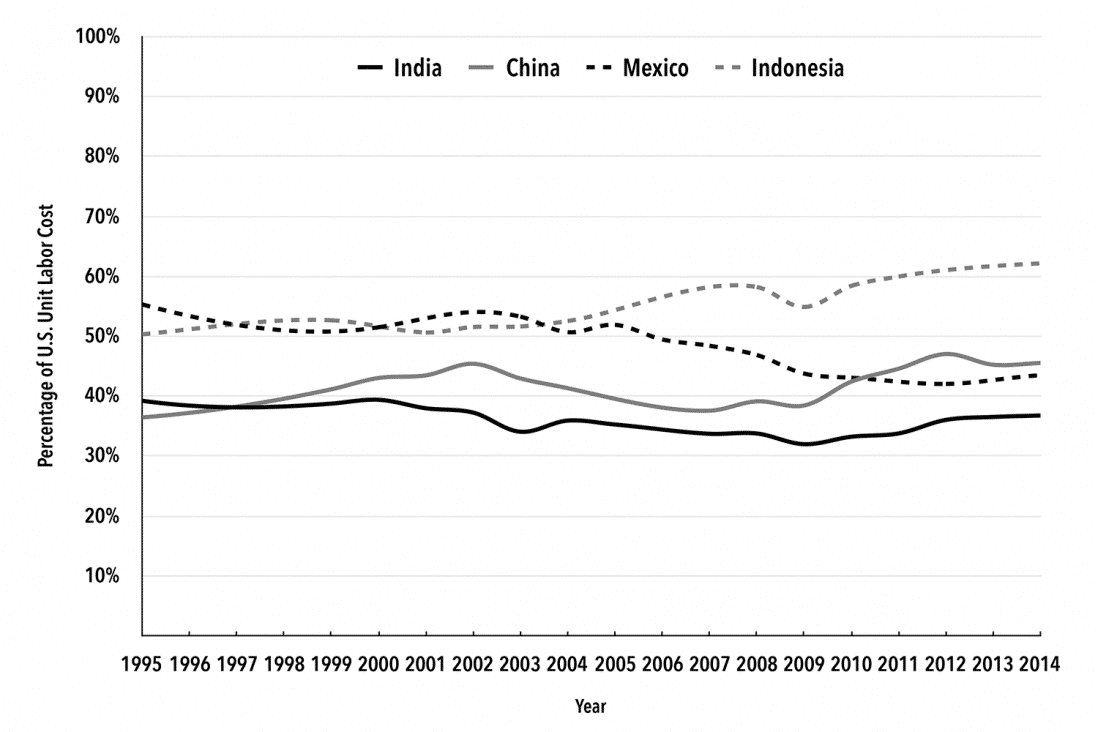

Chart 3 focuses on changes in the unit labor costs in emerging economies in the global South relative to the United States. Over the entire period, unit labor costs in Mexico have declined by 12 percent relative to the United States, reflecting two decades of labor flexibilization, while those of India have remained essentially flat, declining by 2 percent.73 In contrast, those of China and Indonesia have risen by 9 and 12 percent, respectively. India was consistently in the low-cost position, with its unit labor costs in 2014 at 37 percent of the U.S. level, while China and Mexico were at 46 and 43 percent, respectively. Indonesia, despite having the third largest share of global commodity-chain jobs, has unit labor costs in manufacturing that are currently at 62 percent of those in the United States.

Chart 3: Average Unit Labor Cost in Manufacturing Relative to the U.S., Selected Global South Countries, 1995–2014

Sources and Notes: See Chart 2.

It is obvious that other factors besides unit labor costs, such as infrastructure, taxes, primary export country, shipping costs, and finance affect location of critical nodes in commodity chains. Nevertheless, with China’s unit labor costs rising relative to the United States and India’s remaining flat, it is hardly surprising that Apple through its Foxconn subcontractor has recently decided to assemble its top-end iPhones as well as cheaper models in India beginning this year.74 While in 2009 Apple’s gross profit margins on its iPhones assembled in China were 64 percent, rising unit labor costs have clearly cut into these margins.75

The conclusion that much higher profit margins can be obtained through outsourcing production to poorer, emerging economies—when compared to profit margins to be obtained through labor in the wealthy economies at the center—is inescapable.76 All four of the global South countries depicted in this study (China, India, Indonesia, and Mexico) have seen generally flat or declining unit labor costs relative to the United States.

Altogether, the WIOD-SEA data shows clearly why it has been so beneficial—indeed, necessary from the standpoint of profitability—for economies of the global North to maintain substantial parts of their labor-value commodity chains in poor emerging economies. By means of these commodity chains, with their critical nodal points (in terms of labor costs) in low-wage countries, corporations in the North are able to secure low-cost positions essential to their global competitiveness, based on much higher rates of labor exploitation. Here it is important to underscore that a given product, such as an iPod or an iPhone, often has its parts manufactured in a number of different countries, for example, Germany, Korea, and Taiwan, but the assembly occurs in China—a country that has among the lowest unit labor costs and offers developed infrastructure, scale effects, etc.—so it is marked as made in China.77 In other words, while the commodity chain is complex and extended, the country with the lowest unit labor costs tends to be the site of final production/assembly and becomes the most critical node for the enlargement of gross profit margins.78

The above findings reflect the great discrepancy in wages and in unit labor costs between countries in the global North and the global South, as recently as 2014. As Lowell Bryan, director of the New York office of the high-level investor’s publication, the McKinsey Quarterly, stated in 2010:

Any company sourcing its production or service operations in a lower-wage emerging-market country…can save enormously on labor costs.… Even today, the cost of labor in China or India is still only a fraction (often less than a third) of the equivalent labor in the developed world. Yet the productivity of Chinese and Indian labor is rising rapidly and, in specialized areas (such as high-tech assembly in China or software development in India), may equal or exceed the productivity of workers in wealthier nations.79

The way in which the labor-value commodity chains work at the ground level is best illustrated by looking at a particular example, like the Apple iPhone hitherto manufactured in China, which has become the global assembly center for much of modern manufacturing. Most production for export via multinational corporations in China is assembly work, with Chinese factories relying heavily on cheap migrant labor from the countryside (the “floating population”) to assemble products. The main technological components of this final assembly are manufactured elsewhere and then imported into China. Apple subcontracts the production of the component parts of its iPhones to a number of countries, with Foxconn subcontracting the final assembly in China. Due in large part to low-end wages paid for labor-intensive assembly operations, Apple’s gross profit margin on its iPhone 4 in 2010 was found to be 59 percent of the final sales price. The share of the final sales price actually going to labor in mainland China itself was only a fraction of the whole. For each iPhone 4 imported to the United States from China in 2010, retailing at $549, only about $10, or 1.8 percent of the final sales price, went to labor costs for production of components and assembly in China.80

Similar conditions of globalized exploitation, largely hidden in these labor-value commodity chains, pertain to other countries, particularly where multinational corporations rely on subcontractors (or arm’s length production). In the international garment industry, in which production now takes place almost exclusively in the global South, direct labor cost per garment is typically around 1–3 percent of the final retail price, according to senior World Bank economist Zahid Hussain.81

In 1996, a year for which data on the labor-value component of Nike’s commodity chain for its shoes is available, a single Nike shoe consisting of fifty-two components was manufactured in five different countries. The entire direct labor cost for the production of a pair of Nike basketball shoes in Vietnam in the late 1990s, retailing for $149.50 in the United States, was $1.50, or 1 percent.82 As reported by the National Labor Committee and China Labor Watch in 2004, unit labor costs for the production of a pair of sneakers for PUMA, a German multinational, in China in the early 2000s were so low that the hourly profit on each pair of sneakers was more than twenty-eight times greater than the hourly wages workers in China received to make the sneakers.83

A 2019 study published by the Blum Center for Developing Economies at the University of California, which interviewed 1,452 Indian women and girls (including children 17 years old or younger)—85 percent of whom did home-based work “bound for export to major brands in the United States and the European Union”—determined that these workers earn as little as fifteen cents per hour. They “consist almost entirely” of female workers from “historically oppressed ethnic communities” in India, and their work typically involves “finishing touches” like embroidery and beadwork.84

These extremely exploitative economic relations help us understand the reality of labor-value commodity chains and how they relate to the global labor arbitrage. In essence, each node or link within a labor-value chain represents a point of profitability. Each central node, and indeed each link in the chain, constitutes a transfer of value (or labor values). This is partially disguised by conventions with respect to GDP accounting and hence ways of computing value added. In effect, as numerous analysts have now shown, labor values generated by production are “captured” and not registered as arising in the peripheral countries due to asymmetries in power relations, in which multinational corporations are the key conduits.85

Hidden in the pricing and international exchange processes of the global capitalist economy—a reality scarcely captured in traditional commodity-chain or even value-chain analysis—is an enormous gross markup on labor costs (rate of surplus value) amounting to superexploitation, both in the relative sense of above-average rates of exploitation and also, frequently, in the absolute sense of workers paid less than the cost of the reproduction of their labor power. The conditions of political-economic power in relation to the periphery of the world economy feed widening gross profit margins, leading to today’s global overaccumulation. So extreme is this overaccumulation that the twenty-six wealthiest individuals in the world, most of whom are Americans, now own as much wealth as the bottom half of the world’s population, 3.8 billion people.86 Structurally, this level of inequality has become possible as a result of a globalized commodity-chain system of exploitation—a new imperialist division of labor associated with global monopoly-finance capital.

The view, even among some leftist thinkers, that the historic character of economic imperialism is now inverted—with the imperialist relations in the world economy, “largely reversed” to the benefit of the South (East) and at the expense of the North (West)—is based on a very superficial analysis of the growth of emerging economies, particularly China and India.87 The truth is that the world capitalist economy, judged in terms of the amassing of financial wealth and asset concentration, is becoming in many ways more centralized and hierarchical than ever.88 What we are seeing is the emergence of a global wealth pyramid in which the fabled wealth hierarchy of the pharaohs pales into insignificance in comparison. Inequality is increasing in almost all nations as well as between the richest and poorest countries.89 As Oxfam indicates, the issue before us is the question of “an economy for the 99%.”90 In the meantime, imperialism continues to cast its long shadow over the global economy.

An examination of labor-value commodity chains therefore reveals the exploitation hidden in today’s international transactions. The labor-value commodity chains approach acknowledges various components largely missing from the other global-chain frameworks, or not previously brought into systematic relation, namely: (1) global capital-labor relations; (2) the deep wage inequalities between the global North and global South; (3) differential rates of exploitation on which the global labor arbitrage is based; and (4) the phenomenon of value capture. Most importantly, this approach incorporates the labor theory of value as an analytical tool in order to provide a more effective critique of the contemporary global political economy.91 All of this helps us understand how the global commodity chains of monopoly-finance capital—the power configuration behind today’s neoliberal globalization—are rapidly changing class relations and struggles worldwide.

There are other factors besides unit labor costs affecting the profitability of commodity chains and hence the location of production.92 Nevertheless, unit labor costs are the key to unlocking the secrets of the global labor arbitrage and the differences in the rate of exploitation between the global North and the global South.

Through global commodity chains, imperialism enters into the very structuring of production worldwide on a commodity-by-commodity basis. Flexible, globalized production means that the most labor-intensive links in global commodity chains are located in the global South, where the reserve army of labor is larger, unit labor costs are lower, and rates of exploitation are thus correspondingly higher. The result is much higher profit margins for multinational corporations, with the additional value generated often credited to production in the center itself and with the overall process leading to the amassing of wealth in the center, via a kind of profit by expropriation.

As it has become more pervasive, this imperialist exploitation and expropriation has become more disguised and invisible. To understand the nature of today’s economic imperialism, it is therefore necessary to leave the realm of exchange in which so-called free trade is dominant, and enter the “hidden abode of production,” where the existence of extremely high rates of exploitation, revealed by unit labor cost analysis lays bare the very essence of globalized monopoly-finance capital.93

Statistical Appendix

The World Input-Output Database: Socio Economic Accounts (WIOD-SEA) is composed in two distinct (but overlapping) data releases. The 2013 release contains data on forty countries, covering the period between 1995 and 2011.94 The 2016 release contains data on forty-three countries, covering the period between 2000 and 2014.95 Two changes made in the 2016 release are significant for our analysis. First, the 2016 release uses an updated industry classification scheme (ISIC Rev. 4; the 2013 release used ISIC Rev. 3). Second, the variable “Total hours worked by persons engaged” (H_EMP), referring to all workers—as opposed to the more restrictive category of “Hours worked by employees” (H_EMPE)—was dropped.96 Due to the fact that H_EMPE data is spotty for many countries, and entirely unavailable for China, we developed the following technique to calculate key variables in the 2016 release:

- We mapped industry categories from the 2013 dataset to 2016 using the “ISIC Rev. 3—Rev. 4 mapping” table provided by WIOD.97 This resulted in the merging of two ISIC Rev. 3 categories (“Textiles and textile” and “Leather, leather and footwear”) into a single ISIC Rev. 4 category (“Manufacture of textiles, wearing apparel and leather products”). To avoid duplication, we averaged data for these two industry categories then dropped redundant values. In cases where ISIC Rev. 3 industry categories were split into one or more industry categories, only the data for the directly mapped ISIC Rev. 4 industry was used.

- To estimate H_EMP in the 2016 release, we constructed three new variables. We calculated the first two variables from the 2013 release (by country, industry, and year): the ratio of hours worked (H_EMP) to hours worked by employees (H_EMPE), or “hours ratio” for short; and hours worked per worker (H_EMP / EMP), “hours worked.” A third variable was constructed using “Average annual hours worked by persons engaged” (or “average hours worked”) from Penn World Tables. (Data for Hong Kong were used to approximate figures for China.)

- We then merged the variables into the 2016 release (only for the overlapping years 2000–09 in the case of the first two variables) and created estimates using either the H_EMPE variable (hours ratio) or EMP (hours worked and average hours worked). In years where more than one estimate was available, we used the highest figure.98

- Finally, using the 2016 release as a base, we estimated data for 1995–99 using the five-year moving average of annual change in unit labor cost from the 2013 release.99

Unit labor cost is given by the ratio of real “Total labor compensation” (LAB) per hour to “Gross output by industry at current basic prices” (GO) per hour (release 2013: H_EMP; release 2016: estimated H_EMP). Labor compensation (LAB) per hour (H_EMP, as explained above) was converted into 2017 USD using exchange-rate data from Penn World Tables (to convert national currency to USD)100 and inflation coefficients from the economist, Robert Sahr.101 Due to inconsistencies in the data, we dropped figures for the industry “Coke and refined petroleum products” for the United Kingdom. The inconsistency appears to have arisen because there are very few workers in this industry.

Table 2. Manufacturing Industries (ISIC Rev. 4)

| Code | Description |

| C10-C12 | Food products, beverages and tobacco products |

| C13-C15 | Textiles, wearing apparel and leather products |

| C16 | Wood & of products of wood and cork, except furniture; articles of straw & plaiting materials |

| C17 | Paper and paper products |

| C18 | Printing and reproduction of recorded media |

| C19 | Coke and refined petroleum products |

| C20 | Chemicals and chemical products |

| C21 | Basic pharmaceutical products and pharmaceutical preparations |

| C22 | Rubber and plastic products |

| C23 | Other non-metallic mineral products |

| C24 | Basic metals |

| C25 | Fabricated metal products, except machinery and equipment |

| C26 | Computer, electronic and optical products |

| C27 | Electrical equipment |

| C28 | Machinery and equipment n.e.c. |

| C29 | Motor vehicles, trailers and semi-trailers |

| C30 | Other transport equipment |

| C31-C32 | Furniture; other manufacturing |

| C33 | Repair and installation of machinery and equipment |

It should be noted that in presenting average hourly labor compensation data in Chart 2, we convert to U.S. dollars (U.S. = 2017) rather than utilizing “Purchasing Power Parity” (PPP) exchange rates. PPP is important for answering some questions, such as equity and standard of living, but is misleading when approaching other issues, such as international financial flows, the purchase price of labor, profit margins, and the global labor arbitrage. It is the second set of questions that we are concerned with here. As the U.S. Bureau of Labor Statistics says in treating “International Comparisons of Hourly Compensation in Manufacturing,” it is “the cost of labor to an employer, not worker income” that is important.102 The distinction between using PPP and actual market dollars in such computations can be readily understood if we recognize that, according to the ILO’s Global Wage Report 2018/19, “converting all G20 countries’ average wages into US dollars using purchasing power parity (PPP) exchange rate yields a simple average wage of some US$3,250 per month in advanced economies and about US$1,550 per month in emerging economies.”103 Yet, it is obvious that this does not reflect the purchasing price (labor cost) that international capital pays for labor in emerging economies, where wage rates are far below 50 percent of the average wage in the United States and other advanced economies indicated here, quite apart from issues of local purchasing power. As the International Monetary Fund’s Finance and Development journal states, “market exchange rates are the logical choice when financial flows are involved.”104

Notes

- ↩World Bank, “Arms-Length Trade,” Global Economic Prospects (2017), 62, http://pubdocs.worldbank.org; The Impact of Global Supply Chains on Employment and Product System, report no. 1, submitted to the ILO Research Department (Paris: Institut de Recherches Économiques et Sociales, 2018), 8, http://ilo.org.

- ↩American Automobile Labeling Act 2018 (Washington, D.C.: National Highway Traffic Safety Association, 2018), http://nhtsa.gov.

- ↩Nick Vyas, “Four Compass Points for Global Supply Chain Management,” Supply Chain Management Review 22, no. 5 (2018), 5.

- ↩John Bellamy Foster, Robert W. McChesney, and R. Jamil Jonna, “The Global Reserve Army of Labor and the New Imperialism,” Monthly Review 63, no. 6 (November 2011): 4.

- ↩United Nations Conference on Trade and Development (UNCTAD), World Investment Report, 2013 (Geneva: United Nations, 2013), xii.

- ↩World Bank, “Arm’s Length Trade,” 63–64.

- ↩UNCTAD, World Investment Report, 2011 (Geneva: United Nations, 2011), 132.

- ↩World Bank, “Arm’s Length Trade,” 62.

- ↩David Harvey, “A Commentary on A Theory of Imperialism,” in A Theory of Imperialism, Utsa Patnaik and Prabhat Patnaik (New York: Columbia University Press, 2017), 169–71.

- ↩Karl Marx, Capital, vol. 3 (London: Penguin, 1981), 345.

- ↩Stephen Hymer, The Multinational Corporation (Cambridge: Cambridge University Press, 1979).

- ↩Karl Marx, “The Value-Form,” Capital and Class 2, no. 1 (1978): 134.

- ↩The term global supply chain is used by multinationals to refer to the material and logistical aspects of organizing production involving numerous components brought together over spatially dispersed global production platforms. The logistical aspect relates to the old military notion of supply-lines. From a financial-value standpoint, each link in the chain is expected to be profitable and to transfer value toward the center of the system—that is, the multinational itself or its corporate headquarters. Rather than utilize the terms supply chain and value chain, back and forth, we therefore prefer, building on Marxian theory, to refer to commodity chains, or labor-value commodity chains (referring to labor-value chains when the value component is front and center, and commodity chains more generally).

- ↩On unit labor costs and the global capitalist political economy, see John Bellamy Foster, “Monopoly Capital at the Turn of the Millennium,” Monthly Review 51, no. 11 (2000): 1–17.

- ↩On value capture, see John Smith, Imperialism in the Twenty-First Century (New York: Monthly Review Press, 2016), 266–72. One study of value capture written for the Association of Computer Manufacture notes that in arm’s length trading by multinational corporations, value is actually captured (not added). After showing that U.S. companies such as Apple benefit the most even though the production itself is located in China, the analysts end up concluding: “U.S. companies need to work with international partners to bring new products to the market. These companies will capture profits commensurate with the extra value they bring to the table. This is simply the nature of business in the 21st century, and the fact that many U.S. companies are successful in this environment brings significant benefits to the U.S. economy.” Greg Linden, K. Kraemer, and J. Dedrick, “Who Captures Value in a Global Innovation System,” Communications of the ACM 52, no. 3 (2009): 144.

- ↩Financial Flows and Tax Havens (Bergen, Norway: Centre for Applied Research, Norwegian School of Economics and Global Financial Integrity, 2015), 15, https://www.gfintegrity.org; Jason Hickel, The Divide (New York: W. W. Norton, 2017), 24–26, 210–13, 289.

- ↩Nicholas Shaxson, Treasure Islands (New York: Palgrave Macmillan, 2011).

- ↩Costas Lapavitsas, Profiting Without Producing (London: Verso, 2013), 141–47; John Bellamy Foster and Brett Clark, “The Expropriation of Nature,” Monthly Review 69, no. 10 (March 2018): 1–27.

- ↩On value extraction, see Mariana Mazzucato, The Value of Everything (New York: Public Affairs, 2018).

- ↩Samir Amin, “Self-Reliance and the New International Economic Order,” Monthly Review 29, no. 3 (July–August 1977): 1–21; John Bellamy Foster, The Theory of Monopoly Capitalism (New York: Monthly Review Press, 2014), 181.

- ↩Arghiri Emmanuel, Unequal Exchange (New York: Monthly Review Press, 1972), 167.

- ↩Utsa Patnaik and Prabhat Patnaik, A Theory of Imperialism (New York: Columbia University Press, 2017), 196.

- ↩The Impact of Global Supply Chains on Employment and Product System, 11.

- ↩The Impact of Global Supply Chains on Employment and Product System, 8.

- ↩ILO, World Employment and Social Outlook: The Changing Nature of Jobs (Geneva: ILO, 2015), 132.

- ↩Smith, Imperialism in the Twenty-First Century, 101.

- ↩Gary Gereffi, “Global Production Systems and Third World Development,” in Global Change, Regional Response, ed. B. Stallings (Cambridge: Cambridge University Press, 1995), 107.

- ↩Jesus Felipe and Gemma Estrada, “Benchmarking Developing Asia’s Manufacturing Sector,” Asian Development Bank, 2007.

- ↩Karl Marx and Frederick Engels, Collected Works, vol. 36 (New York: International Publishers, 1975), 63; Rudolf Hilferding, Finance Capital (New York: Routledge, 1981), 60.

- ↩Jennifer Bair, “Global Capitalism and Commodity Chains,” Competition and Change 9 (2005): 153–80; Terence Hopkins and Immanuel Wallerstein, “Commodity Chains in the World Economy Prior to 1800,” Review 10, no. 1 (1986): 157–70.

- ↩Gary Gereffi and Miguel Korzeniewicz, eds. Commodity Chains and Global Capitalism (New York: Praeger, 1994).

- ↩See Jennifer Bair, “Global Capitalism and Commodity Chains.”

- ↩Jennifer Bair, “Global Commodity Chains,” in Frontiers of Commodity Chain Research, ed. Bair (Stanford: Stanford University Press, 2009), 1–34. Even that distinction is not clear cut, as some scholars, such as William Millberg and Deborah Winkler, use the global-value/supply-chain framework in a way that is critical of neoclassical transaction cost economics, while being more open to the power dimension associated with commodity-chain analysis, with its Marxian and world system-theory roots.

- ↩Hopkins and Wallerstein, “Commodity Chains in the World Economy Prior to 1800,” 159.

- ↩Immanuel Wallerstein, “Commodity Chains in the World Economy, 1590–1790,” Review 23, no. 1 (2000): 2.

- ↩Gary Gereffi, Miguel Korzeniewicz, and R.P. Korzeniewicz, “Introduction,” in Commodity Chains and Global Capitalism, ed. Gereffi and Korzeniewicz, 2.

- ↩William Milberg and Deborah Winkler, Outsourcing Economics: Global Value Chains in Capitalist Development (Cambridge: Cambridge University Press, 2013).

- ↩Gary Gereffi, “The New Offshoring of Jobs and Global Development,” ILO Lecture Series, 2005, 5.

- ↩Millberg and Winkler, Outsourcing Economics, 12.

- ↩Gereffi, “The New Offshoring of Jobs and Global Production,” 4.

- ↩Gereffi, “Global Production Systems and Third World Development,” 116.

- ↩Gary Gereffi, “The Organization of Buyer-Driven Global Commodity Chains,” in Commodity Chains and Global Capitalism, 99.

- ↩Martin Hart-Landsberg, Capitalist Globalization (New York: Monthly Review Press, 2013), 45.

- ↩Stephen Hymer, The Multinational Corporation (Cambridge: Cambridge University Press, 1979), 43.

- ↩John Bellamy Foster, Robert McChesney, and R. Jamil Jonna, “The Internationalization of Monopoly Capital,” Monthly Review 63, no. 2 (2011): 9.

- ↩John Smith, “Imperialist Realities vs. the Myths of David Harvey,” Review of African Political Economy blog, March 19, 2018, http://roape.net. See also Smith, Twenty-First Century Imperialism.

- ↩Benjamin Selwyn has written about the weakness of current global commodity-/value-chains analyses, both analytical and political, especially due to their failure to “comprehend the nature of capitalist exploitation and indecent work” and to engage in a “bottom-up” perspective on labor. He argues that the crucial task is to reintegrate labor and a solid analysis of capitalism, along with its global class relations, into the studies of global commodity chains. See Benjamin Selwyn, “Social Upgrading and Labour in Global Production Networks: A Critique and an Alternative Conception,” Competition and Change 17, no. 1 (2013): 76; Benjamin Selwyn, “Beyond Firm-Centrism: Re-integrating Labour and Capitalism into Global Commodity Chain Analysis,” Journal of Economic Geography 12: 205–26.

- ↩Stephen Roach, “More Jobs, Worse Work,” New York Times, July 22, 2004.

- ↩Stephen Roach, “How Global Labor Arbitrage Will Shape the World Economy,” Global Agenda Magazine (2004).

- ↩John Smith, “Offshoring, Outsourcing and the Global Labour Arbitrage” (paper delivered to International Initiative for Promoting Political Economy, Procida, Italy, September 2008).

- ↩Smith, “Offshoring, Outsourcing and the Global Labor Arbitrage,” 16.

- ↩Samir Amin, Unequal Development (New York: Monthly Review Press, 1976).

- ↩Karl Marx, Capital, vol. 1 (London: Penguin, 1976), 781–94.

- ↩See Milberg and Winkler, Outsourcing Economics.

- ↩Farshad Araghi, “The Great Global Enclosure of Our Times,” in Hungry for Profit, ed. Fred Magdoff, John Bellamy Foster, and Frederick M. Buttel (New York: Monthly Review Press, 2000), 145–60.

- ↩Mike Davis, The Planet of Slums (London: Verso, 2006).

- ↩Marx, Capital, vol. 1, 795–96, 871.

- ↩James Peoples and Roger Sugden, “Divide and Rule by Transnational Corporations,” in The Nature of the Transnational Firm, ed. Charles N. Pitelis and Roger Sugden (New York: Routledge, 2000), 177–95.

- ↩Foster, McChesney, and Jonna, “The Internationalization of Monopoly Capital,” 12–13.

- ↩Foster, “Monopoly Capital at the Turn of the Millennium,” 7.

- ↩Zak Cope, Divided World, Divided Class (Montreal: Kersplebedeb, 2012), 202.

- ↩ILO, World Employment and Social Outlook, 143.

- ↩See Myron Gordon, “Monopoly Power in the United States Manufacturing Sector, 1899 to 1994,” Journal of Post Keynesian Economics 20, no. 3 (1998): 323–35; Foster, “Monopoly Capital at the Turn of the Millennium.”

- ↩See Foster, “Monopoly Capital at the Turn of the Millennium“; Organisation of Economic Cooperation and Development, OECD Factbook 2014: Economic, Environmental and Social Statistics (Paris: OECD Publishing, 2014).

- ↩Michał Kalecki, Selected Essays on the Dynamics of the Capitalist Economy (Cambridge: Cambridge University Press, 1971), 156–64.

- ↩The G7 countries are Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States. Robert Brenner, “Competition and Class,” Monthly Review 51, no. 7 (1999): 24–44; Robert Brenner, “The Economics of Global Turbulence,” New Left Review 229 (1998): 1–264; Foster, “Monopoly Capital at the Turn of the Millennium.”

- ↩Foster, “Monopoly Capital at the Turn of the Millennium,” 14.

- ↩World Input-Output Database, http://wiod.org.

- ↩Marcel P. Timmer, Erik Dietzenbacher, Bart Los, Robert Stehrer, and Gaaitzen J. de Vries, “An Illustrated User Guide to the World Input-Output Data Base: The Case of Global Automotive Production,” Review of International Economics 23, no. 3 (2015): 575–605.

- ↩Robert C. Feenstra, Robert Inklaar, and Marcel P. Timmer, “The Next Generation of the Penn World Table,” American Economic Review 105, no. 10 (2015): 3150–82.

- ↩Prabhat Patnaik, The Value of Money (New York: Columbia University Press, 2009).

- ↩A final limitation of existing data is the availability of historical figures. The BLS series is by far the longest, going back to 1950 for the U.S. and the 1970s for a handful of other countries; while OECD data is spotty before the 2000s. However, a few researchers have recently developed a methodology for calculating unit labor cost data from the United Nations Industrial Development Organization’s Industrial Statistics Database (INDSTAT). Apart from the availability of historical data, INDSTAT database contains a much larger subset of countries and the figures are specifically on the manufacturing sector. Due to the reasons above, we use this dataset for our research. The INDSTAT data is ideal with respect to our conception of labor-value commodity chains since it allows us to construct a statistically comparable time series (at least back to 1990) for key developed and developing economies. The greater coverage allows us to utilize ILO data on global supply chain participation to follow a theoretically consistent group of counties. See Janet Ceglowski and Stephen Golub, “Just How Low Are China’s Labour Costs?” World Economy 30, vol. 4 (2007): 597–617; Janet Ceglowski and Stephen Golub, “Does China Still Have a Labor Cost Advantage?” Global Economy Journal 12, vol. 3 (2011): 1–28.

- ↩Irma Rosa Martínez Arellano, “Two Decades of Labour Flexibilisation in Mexico Has Left Workers Facing ‘Drastic’ Precarity,” Equal Times, January 30, 2019.

- ↩“Foxconn to Begin Assembling Top-End Apple iPhones in India in 2019,” Reuters, December 27, 2018.

- ↩Foster, McChesney, and Jonna, “The Global Reserve Army of Labor and the New Imperialism,” 15; Yuqing Xing and Neal Detert, How the iPhone Widens the United States Trade Deficit with the Peoples’ Republic of China, ADBI Working Paper, Asian Development Bank Institute (December 2010; paper revised May 2011).

- ↩This recent relative shift in unit labor costs in China and Mexico is familiar in financial circles. See Marc Chandler, “Mexico and China Unit Labor Costs,” Seeking Alpha, January 25, 2017.

- ↩Hart-Landsberg, Capitalist Globalization.

- ↩Unit labor costs are not, of course, the only factor taken into consideration in determining where labor is employed in global supply chains. Other factors include cost factors related to infrastructure and transportation, as well as the absolute quantity of labor available (affected by the size of the labor reserve army in any given locale), language, currency regulations, technology factors, security, etc.

- ↩Lowell Bryan, “Globalization’s Critical Imbalances,” McKinsey Quarterly (2010).

- ↩This and the following paragraph are based on John Bellamy Foster, “The New Imperialism of Globalized Monopoly-Finance Capital,” Monthly Review 67, no. 3 (July–August 2015): 13–14.

- ↩Zahid Hussain, “Financing Living Wage in Bangladesh’s Garment Industry,” End Poverty in South Asia, World Bank, March 8, 2010, http://blogs.worldbank.org.

- ↩Jeff Ballinger, “Nike Does It to Vietnam,” Multinational Monitor 18, no. 3 (1997): 21.

- ↩John Bellamy Foster and Robert McChesney, The Endless Crisis (New York: Monthly Review, 2012), 165–74.

- ↩Siddharth Kara, Tainted Garments: The Exploitation of Women and Girls in India’s Home-Based Garment Sector (Blum Center for Developing Economies at University of California, 2019), 5-9.

- ↩John Smith, “The GDP Illusion,” Monthly Review 64, no. 3 (July–August 2012): 86–102; Smith, Imperialism in the Twenty-First Century, 252–278.

- ↩Larry Elliott, “World’s Richest 26 People Own as Much as Poorest 50%, Says Oxfam,” Guardian, January 20, 2019.

- ↩See Harvey, “A Commentary on a Theory of Imperialism,” 169–71.

- ↩Thomas Piketty, Capitalism in the Twenty-First Century (Cambridge: Cambridge University Press, 2014). See also Michael D. Yates, “The Great Inequality,” Monthly Review 63, no. 10 (March 2012): 1–18.

- ↩Jason Hickel, “Is Global Inequality Getting Better or Worse? A Critique of the World Bank’s Convergence Narrative,” Third World Quarterly 38, no. 10 (2017): 2208–2222.

- ↩Deborah Hardoon, An Economy for the 99% (Oxford: Oxfam International, 2017).

- ↩Samir Amin, Modern Imperialism, Monopoly Finance Capital, and Marx’s Law of Value (New York: Monthly Review Press, 2018); Smith, Imperialism in the Twenty-First Century.

- ↩Jack Nicas, “A Tiny Screw Shows Why iPhones Won’t Be ‘Assembled in the U.S.A.,’” New York Times, January 28, 2019.

- ↩Marx, Capital, vol. 1, 279.

- ↩Abdul Azeez Erumban, Reitze Gouma, Gaaitzen J de Vries, Klaas de Vries, and Marcel P Timmer, WIOD Socio-Economic Accounts (SEA): Sources and Methods (Brussels: WIOD, Seventh Framework Programme, 2012). Note that this release was updated in July 2014—see Reitze Gouma, Marcel P Timmer, Gaaitzen J de Vries, Employment and compensation in the WIOD Socio-Economic Accounts (SEA): Revisions for 2008/2009 and new data for 2010/2011 (Brussels: WIOD, Seventh Framework Programme, 2014). Incidentally, this release effectively ends in 2009 due to major gaps in the availability of variables needed to calculate unit labor cost for the 2010–11 period. The 2013 release is available at http://wiod.org.

- ↩The 2016 release is available at http://wiod.org.

- ↩Capitalized variable names refer to original WIOD-SEA variables, whereas lowercase variables were either generated or estimated.

- ↩Reitze Gouma, Wen Chen, Pieter Woltjer, Marcel P Timmer, WIOD Socio-Economic Accounts (SEA) 2016: Sources and Methods (Groningen, Netherlands: WIOD, 2018), 26.

- ↩It is possible to calculate unit labor costs in the 2016 dataset without making any estimates of total hours worked. The calculation can be carried out by using the ratio of “Compensation of Employees” (COMP) to “Total Hours Worked by Employees” (H_EMPE) in the numerator. This, in fact, yields results that are very similar to those using the ratio of “Total Labor Compensation” (LAB) to “Total Hours Worked by Persons Engaged” (H_EMP). Critically, however, this would mean excluding China entirely, and also removing millions of workers from the calculation, nearly all of which toil in the global South. Indeed, such is the practice of the vast majority of mainstream economists (and institutions) today, who routinely present data on countries like India and China in distinct, non-comparable series—making them appear merely as outliers.

- ↩Apart from China, the two releases produced very similar results. We decided to present the figures in a single chart for the sake of clarity. With that said, it should be emphasized that the WIOD investigators paid special attention to the Great Financial Crisis of 2007-9 in the 2016 release, and that is why we took the effort to use the latter release as our base dataset. See Marcel P. Timmer, Bart Los, Robert Stehrer, Gaaitzen J. de Vries, “An anatomy of the global trade slowdown based on the WIOD 2016 release,” GGDC Research Memorandum (2016).

- ↩Robert C. Feenstra, Robert Inklaar, Marcel P. Timmer, “The Next Generation of the Penn World Table,” American Economic Review 105, no. 10 (2015): 3150–3182.

- ↩Robert Sahr, “2017 Conversion Factors: Individual Year Conversion Factor Tables,” Oregon State University, 2018, http://liberalarts.oregonstate.edu.

- ↩U.S. Bureau of Labor Statistics, “Technical Notes: International Comparisons of Hourly Compensation Costs in Manufacturing,” August 2013, http://bls.gov.

- ↩ILO, Global Wage Report 2018/19 (Geneva: ILO, 2018).

- ↩Tim Callen, “PPP Versus the Market: Which Weight Matters?” Finance and Development 44, no. 1 (2007).